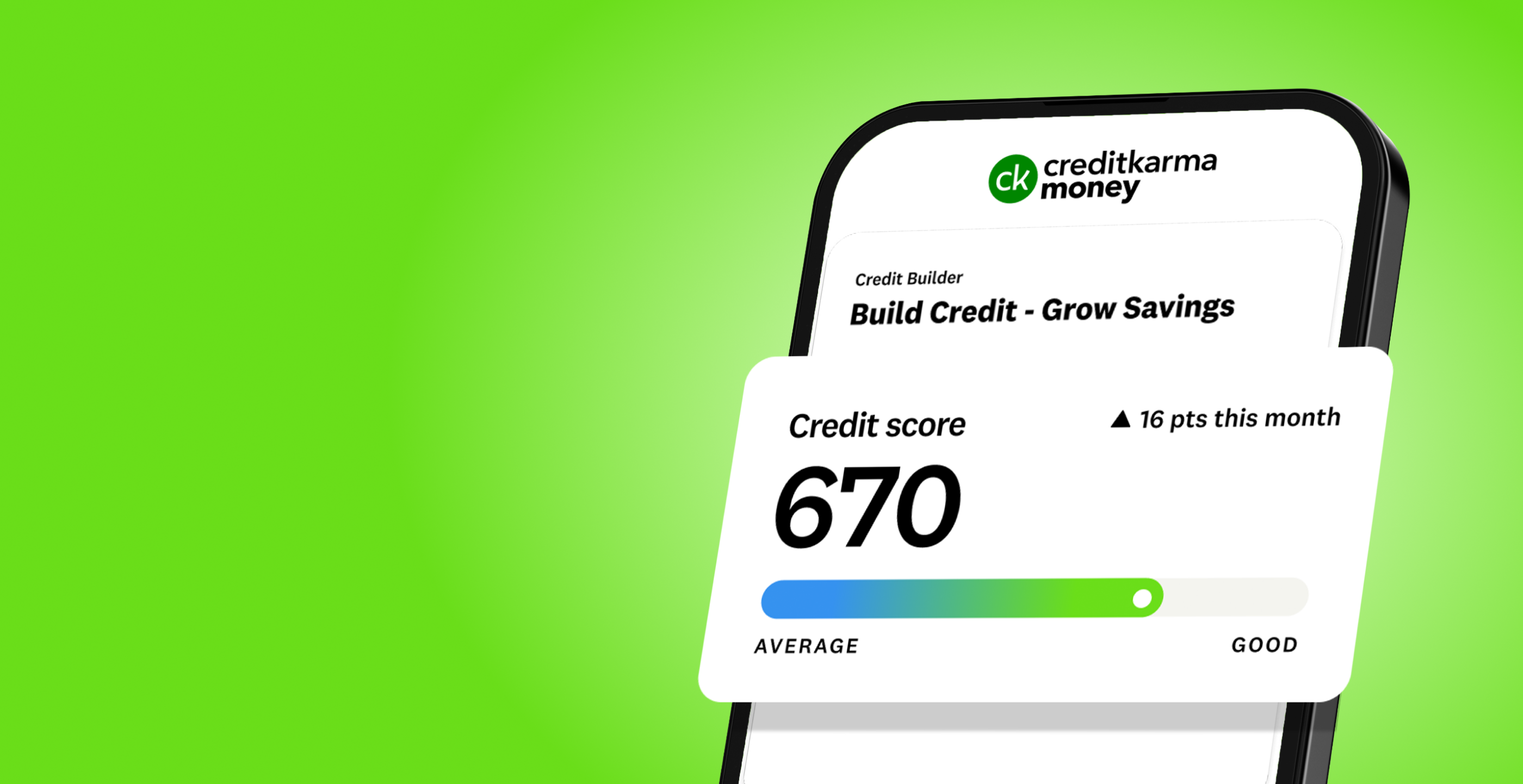

Credit Karma Money™ Credit Builder*

CREDIT

WITH

BOOST

Build credit and savings at the same time.

No credit check. No fees. No gimmicks.

YOU COULD RAISE A LOW SCORE BY AN AVERAGE OF

+17 PTS IN 3 DAYS**

GET STARTED ASAP

Image: Group 2147231660

Image: Group 2147231660Open a Credit Karma Money™ Spend account or link your external bank account.

Image: Group 2147231661

Image: Group 2147231661Choose your amount to contribute, as little as $10 per paycheck.***

Image: Group 2147231659

Image: Group 2147231659We report your payments, which could help grow your payment history.

Image: Group 2147231662

Image: Group 2147231662Your money goes into a locked savings account and once you save $500, we transfer your money back to you.

73M+ POINTS

AND COUNTING

Credit Builder has helped raise thousands of scores and we’re just getting started. Join the movement today.

FAQs

When you open Credit Builder, we open a Credit Builder savings account and line of credit in your name. These banking services are provided by our bank partner, Cross River Bank, Member FDIC. Credit Builder savings account is a deposit product, insured up to $250,000.

You decide how much you want to save each paycheck, and that amount is transferred from your line of credit to your locked Credit Builder savings account every pay period. This transfer is done automatically when you enroll in our optional AutoSave Program or can be manually initiated by you.

Every statement period (which we align to your pay periods), you pay off the total amount of savings you have added from your line of credit to your locked Credit Builder savings account during that period. We report your payments to all three credit bureaus.

Every time you save $500, that amount is transferred to your Credit Karma Money™ Spend account for you to use. Want to use the money to cover expenses? Go for it. Want to keep that $500 safe for a rainy day? Kudos.

The three largest contributors to your credit score are payment history, credit utilization, and account age. Credit Builder utilizes a line of credit to help you save money. Every payment you make to pay off the balance on your line of credit is reported as a payment to the Credit Bureaus. On-time payments to your Credit Builder strengthens your payment history and could help improve credit.

The line of credit that comes with Credit Builder has a limit of $1,000, which increases your overall credit limit, which can result in lower overall credit utilization, and could help build your credit. And finally, the Credit Builder has no fixed term length, so you can keep it active as long as you want. The longer you keep your Credit Builder open, the longer your average account age will be and the more it helps your credit history.

In order to get your Credit Builder plan started, you must Open a Credit Karma Money™ Spend checking account and select how you would like to fund your Credit Builder Savings Account. Choose between (1) linking your external bank account or (2) linking your Credit Karma Money™ Spend account.

Once you’ve decided how much you want to save each paycheck, you can set up the AutoSave Program, which will automatically transfer money from your line of credit to your locked Credit Builder savings account every statement period and will automatically transfer money from your selected account to pay back your line of credit.

We recommend that you set up the AutoSave Program so that you are making automatic contributions to your Credit Builder savings account. Every payment date, AutoSave will pay off your line of credit balance from your linked account. You can always turn off AutoSave or change the linked account before the day of your payment. You can also still make one-time payments without disrupting AutoSave.

If you wish to manually save and make payments, you can initiate them from your linked account in the Credit Karma Credit Builder Account Center once you have your Credit Builder set up. Please note that ACH payments may take 1-2 business days, but payments made before midnight Pacific Time are processed on the same day.

We want to help you to invest in building credit and saving money. Every time you pay a total of $500 towards your Credit Builder savings account, we unlock that amount for you. The $500 is transferred to your unlocked Credit Karma Money™ Spend account. As you keep saving, we keep unlocking your account in $500 increments.

We report on-time payments and your line of credit to the credit bureaus. The more on-time payments you make and the longer you have your Credit Builder active, the more likely it is to help build your credit history. Of course we can’t guarantee that Credit Karma Credit Builder will increase your credit score, but we’re helping set you up for success.

You don’t have to save every month if you don’t want to. One of the advantages of Credit Builder is flexibility. Saving every month will help you reach your savings goal faster and unlock your money faster, but how and when you save is entirely up to you. As long as you keep your account active*, you will be building credit.

*In order to maintain an active account, we require that you use your line of credit to make a transfer to your Credit Builder savings account and pay off your outstanding balance at least once every 3 months after opening.

* Credit Karma is not a bank. Banking services for Credit Karma Money accounts are provided by MVB Bank, Inc, Member FDIC. Maximum balance and transfer limits apply per account. Credit Builder is not provided by MVB Bank.

Credit Builder plan requires you to open a line of credit and a Credit Builder savings account, both banking services provided by Cross River Bank, Member FDIC. Credit Builder savings account is a deposit product, insured up to $250,000. Credit Builder is serviced by Credit Karma Credit Builder. Members with a TransUnion credit score of 619 or below at the time of application may be prompted to apply for Credit Builder. If your score increases over 619, you may no longer see these prompts.

** From June 2024 to November 2024, members with a TransUnion credit score of 619 or below who opened a Credit Builder plan and had it reported on their TransUnion report saw an average credit score increase of 17 points in 3 days of activating the plan. Late payments and other factors can have a negative impact on your score, including activity with your other credit accounts.

*** You may enroll in the optional AutoSave Program, which allows you to automatically save as little as $10 per paycheck if you contribute biweekly or semimonthly and as little as $20 per paycheck if you contribute monthly. If you do not enroll in AutoSave, any contribution you make to Credit Builder may not be less than $10.