Credit Karma Money™ Save

GROW YOUR SAVINGS FASTER

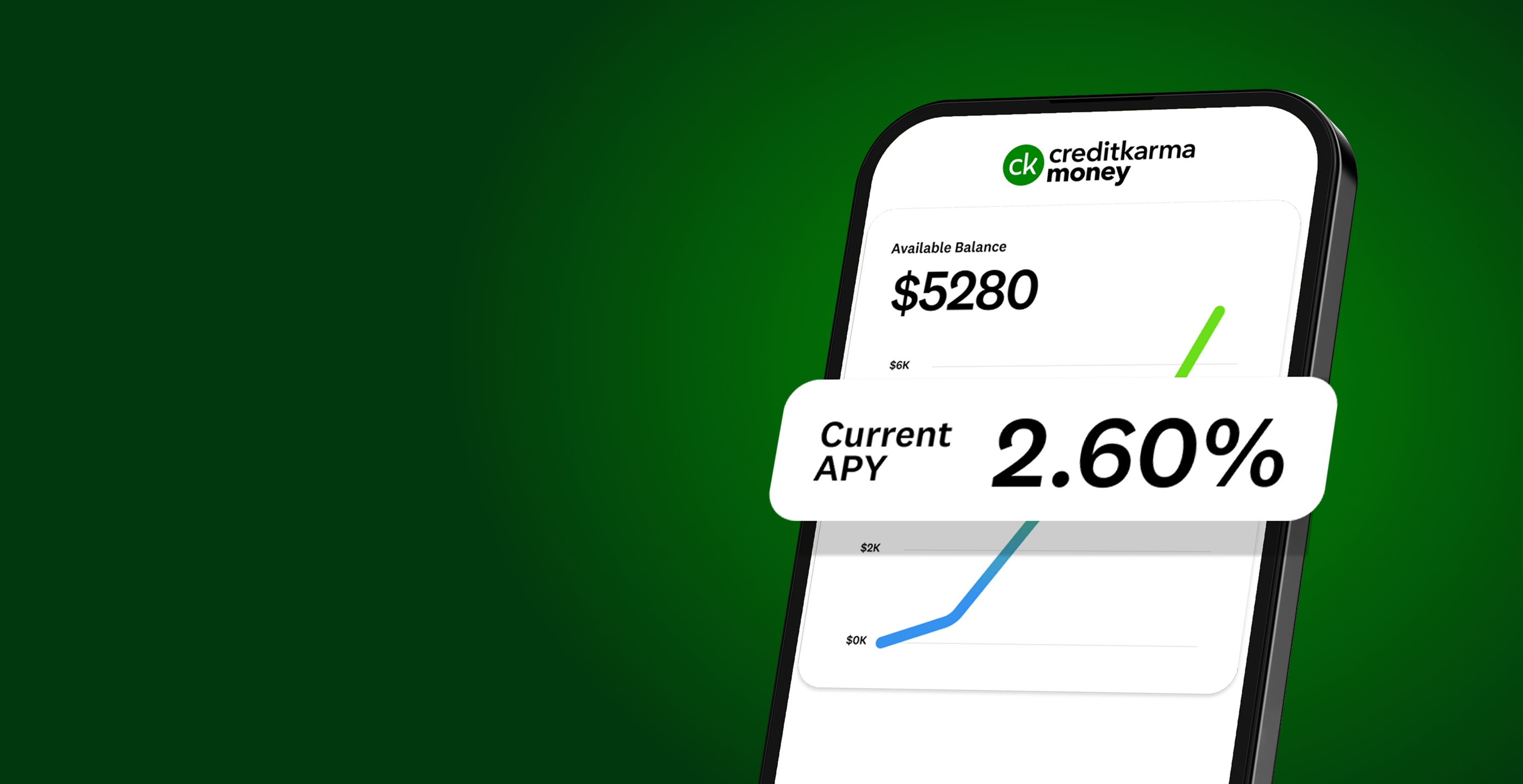

Earn interest on your money with an Annual Percentage Yield (APY) of 2.60%1—6X the national average.2

Credit Karma is not a bank. Banking services provided by MVB Bank, Inc., Member FDIC.

NO FEES OR MINIMUMS

No withdrawal or transfer fees. No minimum balance to open.

FDIC-INSURED

Your money is insured up to $5M through a network of participating banks.3

SAVE YOUR WAY

Add funds yourself or set it and forget it with automatic deposits.

SAVINGS

SUPER-

CHARGED

Level up your savings at 6X the speed with a high-yield Save account4 today.

Open a Credit Karma Money™ Spend account for fast and flexible checking with fee-free Overdraft Coverage5 up to $200.*

*Available with a Qualified Direct Deposit6 of $200 or more.

FAQs

Credit Karma Money offers online checking and savings accounts to help members achieve their financial goals. Accounts are free to open.

Credit Karma is not a bank. We partner with MVB Bank, Inc., Member FDIC, to provide banking services supporting Credit Karma Money Save, a 100% free, interest-bearing savings account with no fees. Your funds are eligible for FDIC insurance3 up to $5,000,000 through a network of participating banks.

There’s never a minimum balance to open and maintain a Credit Karma Money Save account, and there are no hidden fees. And as long as you have at least $0.01 in your Save account, you can start earning interest today.

To open a free Credit Karma Money Save account, you’ll first need to have a Credit Karma account. You can then open a savings account through the Credit Karma app on your mobile device or desktop.

Have more questions? Check out FAQs for Credit Karma Money™ Spend and Credit Karma Money™ Save.

By setting up direct deposit and receiving a single Qualified Direct Deposit (such as payroll, salary, or government benefits) of at least $200 every 35 days, you unlock premium benefits:

– Early Payday: You can receive your paycheck up to 2 days earlier than standard electronic direct deposits,7 and federal government benefits up to 5 days early.8

– Mobile Check Deposit: This mobile-only feature allows you to deposit checks directly into your Spend or Save account by taking a photo of the check in your app.

See our Spend account page for additional FAQs about how Paycheck Advance9 and Overdraft Coverage5 works. At this time we do not offer those benefits for Save accounts.

Credit Karma is not a bank. Banking services provided by MVB Bank, Inc., Member FDIC. Maximum balance and transfer limits apply per account.

1 The Annual Percentage Yield (APY) shown is current as of 11/26/2025. This rate is variable and may change. No minimum deposit to open account. Balance must be at least $0.01 to earn APY. A maximum of 6 withdrawals per monthly statement cycle may apply.

2 Source: FDIC’s national average savings rate as listed at https://www.fdic.gov/resources/bankers/national-rates

3 Credit Karma is not a bank. Through our bank partners, the balance in your savings account may be moved to one or more network banks, as listed here, where it is eligible for FDIC insurance up to $5,000,000 once the funds arrive at network banks. Actual insured amounts may be lower or adversely affected based on any balances you hold in other accounts at other network banks, as each network bank provides up to $250,000 of FDIC insurance coverage per qualified account ownership category. Learn more at: https://www.fdic.gov/deposit/deposits.

4 A maximum of 6 withdrawals per monthly savings statement cycle may apply.

5 One Qualifying Direct Deposit of $200 or more into your Spend or Save account every 35 days to be eligible. Coverage limits range from $20 to $200. No fee to use. Discontinue any time. Overdraft Coverage is discretionary, we may, but are not required to, pay your ACH, debit card and ATM transactions that would have declined due to insufficient funds. Your next deposit will be automatically applied to any negative balance. If your Credit Karma Money Spend account has a negative balance for 60 calendar days or more, it may be closed. Overdraft Coverage does not apply to internal or external transfers. Use responsibly.

6 Qualified Direct Deposit(s) are electronic deposits, of $200 or more into your Spend or Save account every 35 days, for compensation for services, such as payroll, salary, government benefits, or eligible gig/marketplace platform payouts (including rideshare, delivery, and freelance marketplaces) made into your Credit Karma Money Spend or Save account. Person-to-person (P2P) transfers (such as through Venmo, PayPal, or CashApp), transfers from one account to another or from other financial institutions, cash deposits, merchant refunds, one time credits, and Instant Transfers (including Instant Transfers for Earned Wage Access) are not considered Qualified Direct Deposits. Not all electronic deposits qualify, and we reserve the right to determine whether a deposit qualifies based on the information provided with the transaction.

7 Early access to paycheck is compared to standard payroll electronic deposit and is dependent on and subject to payor submitting payroll information to the bank before release date. Payor may not submit payment information early.

8 Early access to federal government benefits is compared to standard electronic deposit and is dependent on and subject to payor submitting benefit payment information to the bank before release date. Payor may not submit payment information early.

9 Paycheck Advance is an optional service subject to approval and eligibility, and is provided by MVB Bank, Inc., Member FDIC. No interest charged and no required fees. Paycheck Advance is not a loan. Limits range from $20–$500. Advance limits and eligibility are evaluated frequently and may change at any time. You must have an active Spend account that has been open for at least 30 days and receive one Qualified Direct Deposit (QDD) of $200 or more to your Spend or Save account within the prior 35 days. Standard delivery is free with funding in 1-2 business days, and if you choose expedited delivery, an Instant Access Fee applies and will be shown before you confirm. You must live and remain in a state where Paycheck Advance is available to be eligible, see State Eligibility. Your advance is automatically repaid from any Qualified Direct Deposit. Terms and Conditions apply. Use responsibly.