Just in time for the holidays, the latest move by the Federal Reserve could bring the gift of lower rates on such things as auto financing, mortgages and personal loans.

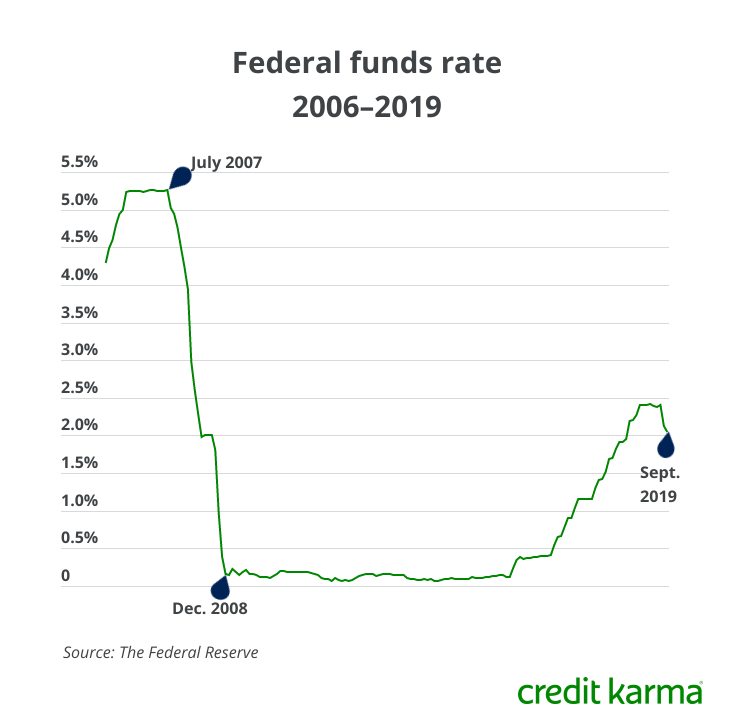

Following its meeting this week, the Fed again cut the federal funds rate by 0.25% — the third time in 2019 — to a rate between 1.5% and 1.75%. Although the Fed cut rates twice over the summer, many had expected this third rate cut because of ongoing economic uncertainty.

This rate cut could signal lower rates ahead if you plan to buy a home or vehicle, for example, refinance a mortgage or take out a personal loan. But if you’ve got a high-yield savings account, you may see the interest rate fall slightly. Read on to learn more.

Want to know more?

Wait, why is the Fed still cutting rates?

You might be wondering why the Fed is cutting rates so soon after its last rate cut in September. After all, the three Fed rate cuts since July marked the first reductions in years. However, Fed officials are likely still concerned about business investment and the ongoing U.S.-China trade dispute. The issues affecting the economy over the summer likely haven’t improved as much as the Fed would like to see.

Still, there’s an indication that the Fed may be nearing the end of its string of rate cuts and adopting a “wait-and-see” approach. At the latest meeting, eight policymakers voted for the rate cut, while two voted to keep rates steady. And in their latest policy statement, Fed officials said they’d keep an eye on economic data to assess “the appropriate path” for rates.

What could this latest rate cut mean for you?

You might not notice any change unless you’ve been shopping around for an auto loan, personal loan or mortgage. You could see lower interest rates on loans now than when you looked at rates a couple of weeks ago.

Any loans or lines of credit you currently have may be affected — it mainly depends on whether you have a fixed or a variable APR. So now is a good time to check your terms to get an idea of whether you’ll see any changes. It could also potentially be a good time to refinance.

At the same time, if you’ve got a savings account, it’s possible you’ll see lower interest rates on that account. If you haven’t already, you may want to consider a high-yield savings account so you can earn a bit more interest on your savings than with a traditional savings account.

If you want to keep up with what the Fed might be planning for interest rates, you can follow its meeting calendar and statement releases here.