Americans’ total savings have grown a lot following the 2008 recession, according to U.S. Department of Commerce data. In fact, 2019’s savings rate is shaping up to be the highest average savings rate since 2012.

That data may be a little misleading, though.

A number of economists say it’s likely that the wealthiest fraction of Americans, along with Baby Boomers facing retirement, are responsible for most of the saving.

Read on to learn more about how this rise in savings may reflect a widening gap between those who can afford to grow their savings and those who can’t — and how a higher rate of savings may affect the economy overall.

Want to know more?

What’s going on with Americans’ savings?

In its report on the Economic Well-Being of U.S. Households in 2017, the Federal Reserve reported that 4 in 10 adults didn’t have enough cash set aside to handle a $400 emergency.

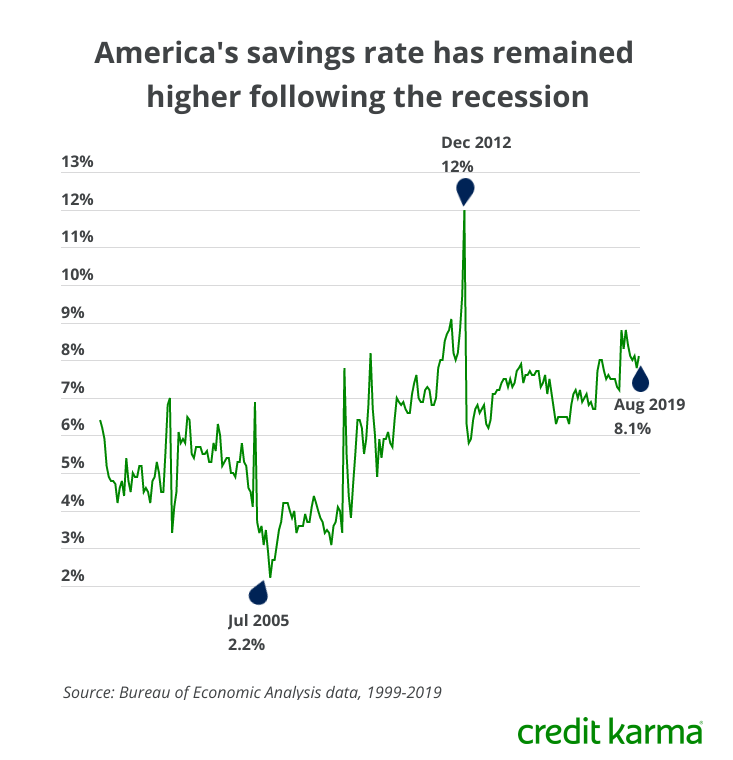

Yet the chart below, based on data from the Bureau of Economic Analysis, indicates that savings began increasing in mid-2005, near the end of a period of economic growth — and that savings rates have generally continued to increase since 2010, after the recession ended.

Analysts have a few theories to explain what’s happening, according to a report in the Wall Street Journal.

- The wealthy are driving savings growth: As the Journal reports, the fact that savings are up overall following 2018’s tax cuts is probably not a coincidence. Moody’s Chief Economist Mark Zandi estimates that 75% of the savings growth that’s happened since the tax cut has come from the wealthiest 10% of Americans saving more. According to a Congressional Research Service report, higher-income folks were the biggest beneficiaries of the Tax Cuts and Jobs Act and more likely to save the windfall.

- People are uncertain about the economy: The Federal Reserve cut rates twice this year in response to a more uncertain outlook for the economy, and consumer confidence may be shaky as a result. People may feel more compelled to hold onto their money rather than spend it if they’re worried about the future.

- A lot of people are facing retirement: Baby Boomers are at or near retirement. This may mean many Americans are growing more conservative with the money they have because they’re worried about having enough retirement savings.

The long-term impact of a high rate of savings rather than spending could be slower economic growth. The GDP (gross domestic product) — a key measure of how the economy is doing — is a reflection of how much people are spending on goods and services.

What should you do?

Consider using this news as an opportunity to think about setting a budget that includes a plan for savings. By planning now, you may be able to better prepare for the future no matter where the economy heads.

Most people probably can’t put away several months’ worth of emergency funds immediately. If that’s the case for you, don’t get discouraged. Saving as much as you can to create a starter emergency fund of around $500 to $1,000 can help protect you financially from smaller bumps in the road — and can set you on a path toward bigger savings and stability down the road.